The company owes $10,999 after this payment, which is $21,474 – $10,475. The company owes $21,474 after this payment, which is $31,450 – $9,976. The company owes $31,450 after this payment, which is $40,951 – $9,501.

Payment of interest on notes payable

A review of the time value of money, or present value, is presented in the following to assist you with this learning concept. N/P is an additional credit source for businesses aside from accounts payable. It can delay payments for purchases or loans, which gives businesses more flexibility in managing their working capital. However, it has interest charges, which are an additional expense for the borrower.

- If a debtor runs into financial difficulties and is unable to pay, or fully repay, the note, the estimated impaired cash flows become an important reporting disclosure for the lender.

- Another problem with issuing a note payable is it increases the organization’s fixed expenses, and this leads to increased difficulty of planning for future expenditures.

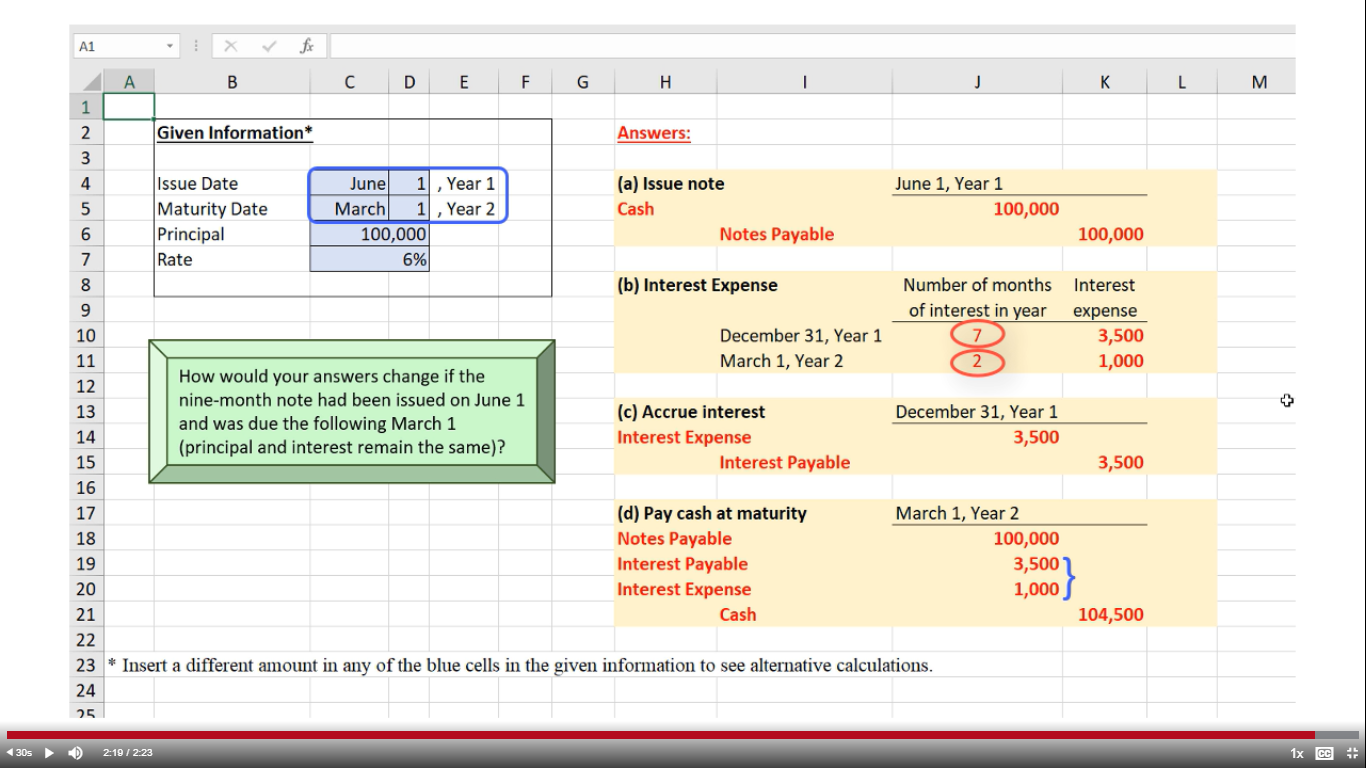

- Let’s look at what entries are passed in the journal for notes payable.

- This payable account would appear on the balance sheet under Current Liabilities.

- The land has a historic cost of $5,000 but neither the market rate nor the fair value of the land can be determined.

- Also, the process to issue a long-term note is more formal, and involves approval by the board of directors and the creation of legal documents that outline the rights and obligations of both parties.

Parties Of Note Payable

These agreements detail all important points surrounding the transaction. It comprises information related to the amount paid, applicable interest rate, name of the payer and payee, the maturity date, limitations if any, and the issuer’s signature with the date. In addition, the timeframe can differ hugely and range from a few months to five years or maybe more. In short, these promissory notes can be short-term with a validity of up to a year or long-term, involving a timeframe of more than a year, given the period of payment and repayment involved. Notes payable is a promissory note that represents the loan the company borrows from the creditor such as bank.

Recording Short-Term Notes Payable Created by a Loan

A business may borrow money from a bank, vendor, or individual to finance operations on a temporary or long-term basis or to purchase assets. Note Payable is used to keep track of amounts that are owed as short-term or long- term an overview of the american opportunity tax credit business loans. Notes payable are initially recognized at the fair value on the date that the note is legally executed (usually upon signing). Subsequent valuation is measured at amortized cost using the effective interest rate.

Notes Payable Issued to Bank

It can be three months, six months, one year, or as the parties consider feasible. Short-Term Notes Payable decreases (a debit) for the principal amount of the loan ($150,000). Interest Expense increases (a debit) for $4,500 (calculated as $150,000 principal × 12% annual interest rate × [3/12 months]).

Balance Sheet

It has agreed-upon terms and conditions that must be satisfied to honor the agreement. However, the account payables are informal records, and the terms & conditions are not rigid. Since they’re not written agreements, the terms can be changed on the agreement between the vendor and the business entity. If the borrower decides to pay the loan before the due date of the note payable, the computation of interest will not be done for the pre-decided period.

Notes Payable are a promise in writing whereby a borrower assures repaying the lenders within a specific period. These promissory notes indicate the loan that one party lends to the other, expecting the timely repayment, which may be the principal alone or the principal along with the interest amount. Notes payable is a liability account that’s part of the general ledger. Businesses use this account in their books to record their written promises to repay lenders.

This shorter payback period is also beneficial with amortization expenses; short-term debt typically does not amortize, unlike long-term debt. The goal is to fully cover all expenses until revenues are distributed from the state. However, revenues distributed fluctuate due to changes in collection expectations, and schools may not be able to cover their expenditures in the current period. This leads to a dilemma—whether or not to issue more short-term notes to cover the deficit.

Amortized agreements are widely used for property dealings, be it a home or a car. These contracts are obligations for the parties involved and are classified as – single-payment, amortized, negative amortization, and interest-only types. Therefore, exploring them is important to better understand the meaning of notes payable. Businesses with high transaction volumes or those that need daily oversight of their finances should record entries daily.

This includes the journal entry for the initial recognition as well as subsequent installment payments and accrued interest expense. Long-term notes payable are often paid back in periodic payments of equal amounts, called installments. Each installment includes repayment of part of the principal and an amount due for interest. The principal is repaid annually over the life of the loan rather than all on the maturity date. As mentioned above, at the initial recognition, the long-term notes payable are recorded at its selling price or at its face value minus any discount or premium on the notes. For simplicity, we will illustrate only the notes sold at their face value.

There are usually two parties involved in the notes payable –the borrower and the lender. The borrower is the party that has taken inventory, equipment, plant, or machinery on credit or got a loan from a bank. On the other hand, the lender is the party, financial institution, or business entity that has allowed the borrower to pay the amount on a future date. There is an ebb and flow to business that can sometimes produce this same situation, where business expenses temporarily exceed revenues. Even if a company finds itself in this situation, bills still need to be paid.